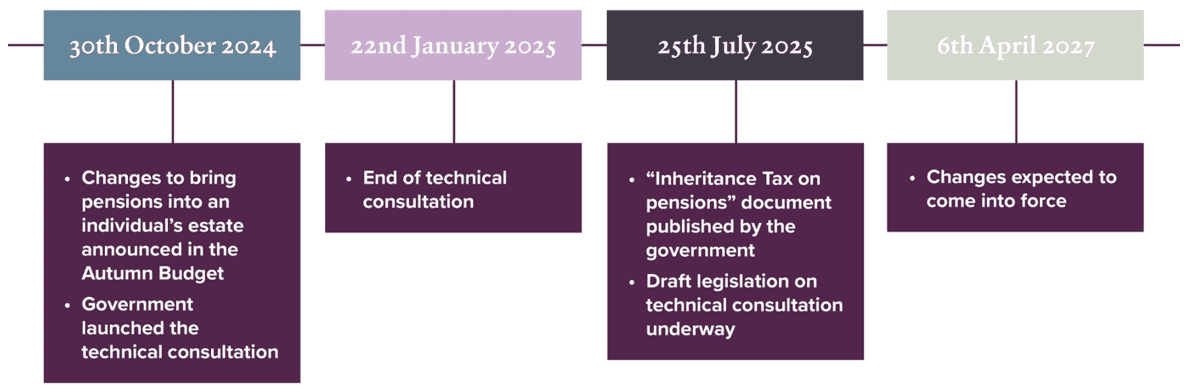

In the 2024 Autumn Budget, Chancellor Rachel Reeves announced significant changes affecting pensions and Inheritance Tax (IHT).

Designed to “deliver a fairer and less economically distortive tax treatment of inherited wealth and assets”, from 6 April 2027, “unused” pension funds and death benefits will be included in an individual’s estate upon death.

As such, pension savings will become subject to IHT at a rate of 40% on amounts exceeding the nil-rate band.

Current rules v incoming changes

Under existing rules, if a pension scheme member dies before age 75, the remaining pension benefits can be paid out as income to beneficiaries tax-free, regardless of the amount, and beneficiaries do not need to be dependants.

While they aim to continue to encourage people to use pensions to save for retirement, by removing the incentive for use as a tax-efficient way to transfer wealth after death, the government hopes to align pension tax treatment with other types of inherited assets.

Inheritance Tax on pensions timeline

The changes are scheduled to come into effect from April 2027.

So, you still have time to review and adjust your estate plan accordingly.

If you’re concerned about how the changes may affect you and your beneficiaries, we’re here to explain more and explore potential avenues that might help you to mitigate any potential tax charge on your estate.

Pension death benefits affected

Most types of pension schemes will be affected by the change – with two notable exceptions: for dependants’ scheme pensions (which remain subject to Income Tax) and charity lump sum death benefits.

Importantly, spousal exemptions will continue to apply, meaning that death benefits paid to a spouse or civil partner will not attract IHT.

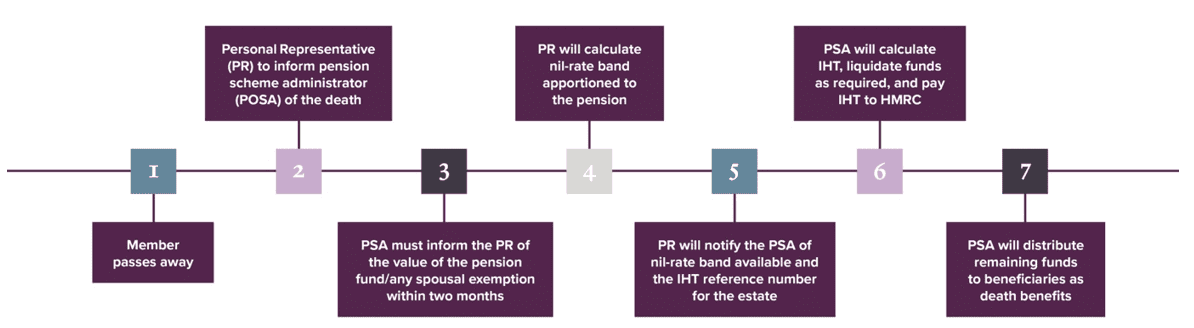

Proposed process for Inheritance Tax payment

The proposed process involves several steps to be completed within six months of the individual’s death to avoid late payment interest.

This includes the Pension Scheme Administrator (PSA) assessing and paying the IHT liability.

After 12 months, the liability may become jointly held between the PSA and the beneficiary, allowing HMRC to pursue repayments directly from beneficiaries if adjustments are made after benefits have been distributed.

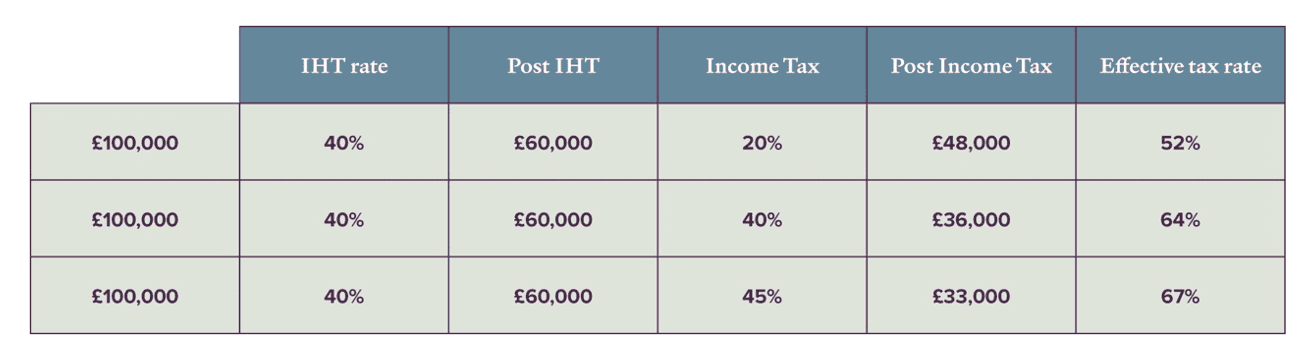

Effective tax rates

The combination of IHT and Income Tax on distributed pension funds could result in substantial effective tax rates for beneficiaries.

For example, a taxable pension fund of £100,000 could incur an effective tax rate ranging from 52% to 67%, depending on the Income Tax bracket of the beneficiary, on death after age 75.

Meanwhile, should your estate exceed £1 million, a pension pot worth £500,000 could face a £200,000 IHT charge. And larger estates could be hit even harder.

This is because when your estate surpasses £2 million, the residence nil-rate band (RNRB) begins to taper away – at a rate of £1 for every £2 an estate exceeds £2 million.

Once an estate reaches £2.35 million RNRB tapers away completely, exposing beneficiaries to even greater IHT charges.

There’s still time to revisit your estate plan

If you’ve worked hard to build a pension pot, whether for a comfortable retirement or to leave a legacy, it’s worth revisiting your estate plan in light of these changes.

While tax-relieved contributions and tax-free growth continue to provide considerable advantages, if you’re unlikely to use large pension funds during your lifetime, you may wish to consider drawing income and making gifts during your lifetime.

Using your annual gifting allowances, for instance, and/or making regular gifts out of income may prove an effective way to reduce or remove any potential IHT liabilities on your estate.

Read more: 5 ways to avoid being caught out by Inheritance Tax

Last year, Brits were hoping for positive changes to IHT.

Now, on top of the changes to Business Property Relief, AIM shares, and Agricultural Relief that are coming into force in April 2026, it appears that the country’s “most hated tax” is likely to remain on the agenda for the foreseeable future.

Get in touch

At KBA, we’re committed to guiding our clients through these complex changes. And we invite you to attend our upcoming IHT Webinar on Monday 6 October at 5 pm.

Hosted by our Company Director & Chartered Financial Planner, Sarah Hogan, the session is designed to give you clarity, confidence, and peace of mind when it comes to planning for the future.

Meanwhile, for personalised advice and to discuss how these changes may impact your estate planning, please email contactme@kbafinancial.com or call us on 01942 889 883.

Please note

This article is for general information only and does not constitute advice. The information is aimed at retail clients only.

All information is correct at the time of writing and is subject to change in the future.

The value of investments and any income from them can fall as well as rise and you may not get back the original amount invested.

HM Revenue and Customs’ practice and the law relating to taxation are complex and subject to individual circumstances and changes which cannot be foreseen.

Approved by The Openwork Partnership on 17/09/2025.