Earning £100,000 or more each year should be a good measure that you’re winning at life, but, in the UK, a six-figure salary can present several issues that could prove costly.

An article in MoneyWeek reveals that more than 2 million Brits are expected to earn £100,000-plus in the 2026/27 tax year.

If you’re among this number, you’re likely paying tax at an effective rate of 60%.

The good news is there are measures you could take to reduce the tax you pay and keep more of your hard-earned wealth.

How earnings over £100,000 end up being taxed at 60%

Let’s start with the basics.

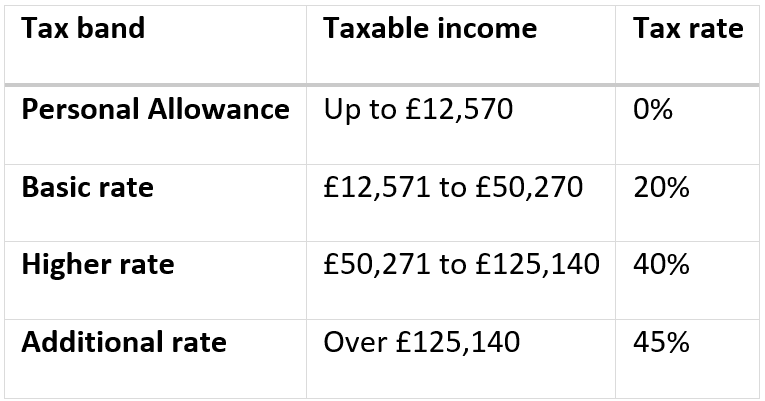

In the UK, the amount of Income Tax you pay depends on how much you earn. The table below shows you the Income Tax rates for the 2026/27 tax year:

If you earn £60,000 a year, you’d typically pay:

- 0% tax on your income below the tax-free Personal Allowance (£12,570)

- 20% tax on £37,700

- 40% tax on £9,730.

While the highest rate of Income Tax appears to be 45% for earnings that exceed £125,140, there’s a costly catch… because for every £2 that your earnings exceed £100,000, you lose £1 of your Personal Allowance.

As a result, if you’re an additional-rate taxpayer with earnings over £125,140, you lose your Personal Allowance altogether – which means all your earnings are taxed.

And this is how you end up paying tax at an effective rate of 60% – no wonder it’s widely called the “60% tax trap”!

Parents earning over £100,000 could lose free childcare benefits

Providing both parents are working, the Free Childcare for Working Parents scheme allows up to 30 free hours of childcare a week for children between nine months and four years.

However, if either you or your partner earns more than £100,000 a year, you could lose out on much of the possible support. Instead, your child might receive just 15 hours a week free, and only between ages three and four.

According to The Week, losing this free childcare entitlement could cost £9,600 a year for each child.

Meanwhile, figures from the Institute for Fiscal Studies show that a parent with two children (living outside London) would need to earn £137,000 before they had as much disposable income as when they earned £99,000.

Your total income counts, not just your salary

It’s not only your salary that counts towards your Income Tax calculation.

Any ad hoc earnings, such as bonuses, could also tip you into the tax trap. So, if you receive a bonus that takes your income over £100,000, you could effectively pay 60% tax on any of it between £100,000 and £125,140.

As well as bonuses, your adjusted net income can also include:

- Profits from self-employment

- Interest on savings

- Income from a trust

- Rental income

- Pension income

- Some state benefits.

As such, you may need to keep an eye on your total annual income to ensure you don’t accidentally breach the £100,000 mark and fall into the 60% tax trap.

Proactive steps that could help you mitigate the 60% tax trap

If you’re caught in the tax trap, here are a few financial planning options to consider.

Boost your pension contributions

Increasing your contributions could help keep your annual adjusted net income below £100,000. Not only that, but paying more into your pension could increase the amount of tax relief you can claim.

For instance, if you usually earn £100,000 and receive a £15,000 bonus, paying your bonus straight into your pension has three benefits:

- Your adjusted income doesn’t breach £100,000

- You still benefit from the full Personal Allowance

- You can claim 40% tax relief on your contribution.

Increasing your pension contributions could also allow your pension pot more potential to grow through compound investment returns. Plus, your employer may be willing to match your contributions, increasing your pot further still.

Join your workplace salary sacrifice scheme

Salary sacrifice allows you to exchange part of your salary for employer-paid benefits.

Your employer reduces your salary “at source” before Income Tax and National Insurance (NI) are calculated. This lessens your Income Tax and NI contributions, reducing your earnings, which could help you to fall below the £100,000 tipping point.

While increased pension contributions are a popular choice, depending on the scheme, you might instead sacrifice your salary for things like:

- Increased holiday entitlement

- Company car

- Childcare vouchers

- Gym membership.

Not all salary sacrifice options offer the potential to reduce your adjusted net income, so if this is something you’re considering, please get in touch and we’ll help you understand all your options.

Alternatively, if you run your own business, you could consider adapting how you extract income.

You may, for example, decide you prefer to draw more through dividends. This could help as Dividend Tax is usually slightly less than Income Tax. You could also benefit from the annual tax-free Dividend Allowance, which is £500 in the 2026/27 tax year.

Make charitable donations

The UK’s Gift Aid scheme allows you to reclaim a percentage of tax from charitable donations.

While charities and community amateur sports clubs can claim an extra 25p for every £1 you give, you can reclaim 20% (for higher-rate taxpayers) or 25% (for additional-rate taxpayers) of the value of your donation.

Helpfully, this reduces your tax liability and makes your contribution go further.

To qualify, donations you make in any tax year must not be more than four times the amount of tax you paid.

If you’re interested to find out more about this or other ways to incorporate charitable giving into your financial plan, please get in touch.

Join our next webinar, designed specifically for high earners like you

Next month (June 2026), we’re running a webinar where we’ll discuss all the potential tax costs for high earners and financial planning tips to help you keep more of your hard-earned wealth.

As well as explaining more about the ideas suggested in this article, we’ll also outline other tax-efficient planning and investment options that could strengthen your long-term financial security.

Alternatively, if you’d like to cut to the chase and talk specifics about how you might be able to better protect yourself from falling into the 60% tax trap, we’d be delighted to hear from you.

To find out more or register your interest in joining the next webinar, please email contactme@kbafinancial.com or call us on 01612602002.

Please note

This article is for general information only and does not constitute advice. The information is aimed at individuals only.

All information is correct at the time of writing and is subject to change in the future.

HM Revenue and Customs’ practice and the law relating to taxation are complex and subject to individual circumstances and changes which cannot be foreseen.

The value of investments and any income from them can fall as well as rise and you may not get back the original amount invested.

Workplace pensions are regulated by The Pensions Regulator.

For specialist tax advice, please refer to an accountant or tax specialist.

Approved by The Openwork Partnership on 06/05/2026.