Rules surrounding Inheritance Tax (IHT) can be confusing at the best of times. If you have financial ties in the UK and abroad, residency and domicile rules add a further layer of complexity.

Historically, IHT has been levied on an individual’s estate when they are UK-domiciled. In simple terms, if you lived in the UK but consider another country your permanent home, you could avoid IHT on assets located outside the UK.

However, from 6 April 2025, the extent to which your worldwide estate is subject to IHT will be based on where you’ve been living in the years before your death. If you’ve been UK tax resident for 10 of the last 20 tax years, you may find that your worldwide estate is liable to IHT.

So, now may be a good time to revisit your estate plan.

The non-dom tax regime is being phased out

If you live in the UK but were born outside the country, or are British but spend the majority of your time living abroad you may qualify as a non-dom. However, the criteria for determining residency have been revised.

The new rules state that:

- Brits and previous UK residents living abroad who claim domicile in another countrymust be a foreign resident for a minimum of 10 years before their non-UK assets fall outside the scope of UK tax. Plus, all UK-based assets will remain within the scope of UK IHT.

- New arrivals to the UK will be exempt from tax on foreign earnings for the first four years of living in the UK. After being in the country for four years, they will then be taxed in the same way as other UK residents.

- Existing non-doms have a three-year transition period – during this time they’ll be encouraged to bring their wealth into the UK.

From 6 April 2025, all UK residents will be taxed on their worldwide income and gains, regardless of their domicile status.

As such, if you’re non-domiciled or have international assets, it’s important to understand how the new rules may affect your financial plan.

New rules could affect Inheritance Tax planning for non-doms and British expats

In the 2024 Autumn Budget, Labour introduced reforms that could change how British expats manage their IHT liabilities.

Most notably, from April 2027, pensions will be brought into the scope of IHT. So, if you have a UK pension but live abroad, you may wish to consider transferring your pension overseas to help mitigate your future IHT liability.

Read more: An Autumn Budget change that might affect your pension savings and estate plan

British expats and previous UK residents could both be affected by the reforms. Here’s what you need to know.

The new rules replace the concept of domicile with long-term residence

Ultimately, if you’ve lived outside the UK for at least 10 of the last 20 years you will now be classified as a non-UK long-term resident (LTR).

If you’re a non-UK LTR, assets you hold outside the UK will not be liable for IHT in the UK, but any assets you hold in the UK – savings, investments, pensions, or property (including land) – will be.

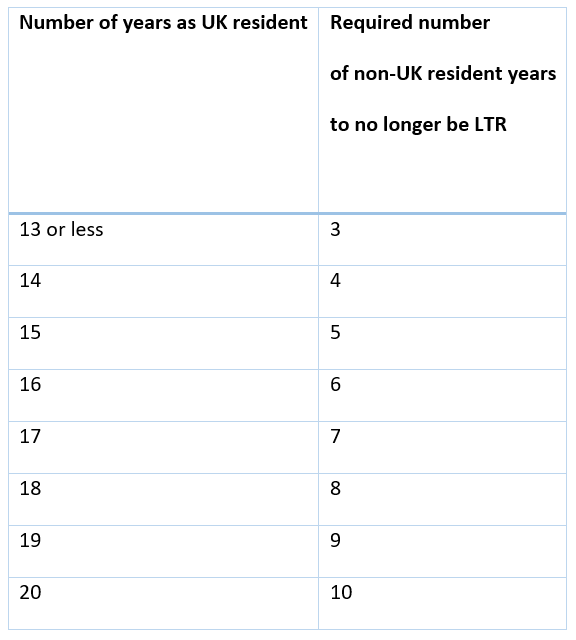

That said, it is possible to move outside the scope of IHT after a consecutive period of non-UK residence.

For example, if you’ve been a UK resident for 10 to 13 years, you must be non-UK resident for three years to fall outside of the scope of IHT.

The table below shows how the number of years you’ve been UK resident affects your non-UK resident status:

Whether you’re an expat or considering moving abroad, you may benefit from restructuring your assets and revisiting your long-term financial plan. Doing so could help you to optimise tax efficiency and mitigate the eroding effects of IHT.

We can help you understand how you could protect your estate from Inheritance Tax

Protecting your estate begins with good planning, and we can help.

From spending more to gifting money during your lifetime, we’ll help you understand all your options, depending on your circumstances and goals.

Trusts may also provide an appropriate way to shield your wealth from IHT, allowing you to pass more to your family and loved ones.

There are several different types of trust you could use to protect and preserve your assets. It’s important that these are structured correctly. We’ll help you work out if they may present a suitable solution for you and your family.

Get in touch

If you’re concerned about how these new rules may affect you, please get in touch. We’ll explain everything in more detail, and help you understand what steps you could take to protect your wealth for future generations.

Email contactme@kbafinancial.com or call us on 01942 889 883.

Please note

This article is for general information only and does not constitute advice. The information is aimed at retail clients only.

All information is correct at the time of writing and is subject to change in the future.

HM Revenue and Customs’ practice and the law relating to taxation are complex and subject to individual circumstances and changes which cannot be foreseen.

The Financial Conduct Authority does not regulate estate planning, tax planning, or trusts.

Approved by The Openwork Partnership on 16/04/2025.