High inflation means retirees could need to increase their budget by almost 20% to maintain the same lifestyle, research suggests. If you’re drawing an income from your pension, it’s vital you understand whether withdrawing more is sustainable.

The UK experienced high inflation throughout much of 2022, and inflation remains above the Bank of England’s target of 2%. This has stretched many household budgets, but retirees may find it more difficult to weather a period of high inflation.

As your income may not increase, or you deplete assets more quickly, you could face more financial uncertainty later in life.

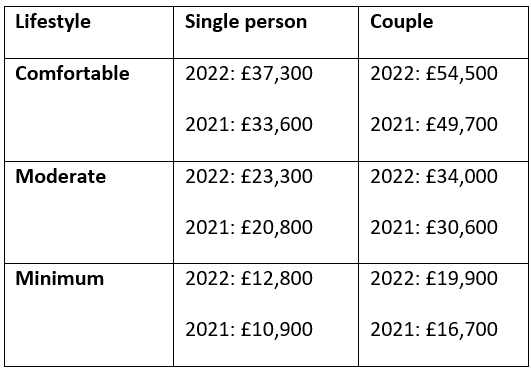

A retired couple needs an annual income of £34,000 for a “moderate” lifestyle

The Pensions and Lifetime Savings Association (PLSA) has updated its Retirement Living Standards to reflect recent high inflation. It found that some retirees will need to increase their budget by 19% just to maintain the same standard of living they enjoyed at the start of 2022.

The organisation noted that people that retired with a lower income have seen the biggest percentage increase because a higher proportion of their budget goes towards areas that have risen the most, such as food and energy.

The PLSA research sets out the annual income retirees may need to secure a “minimum”, “moderate”, or “comfortable” lifestyle.

The “minimum” lifestyle covers things retirees need to live a fulfilling life, including social and cultural participation. For a couple, this includes £96 a week for grocery shopping, a week-long break in the UK, and affordable leisure activities twice a week. It also considers things like maintaining a property.

In the space of just a year, the cost of a minimum lifestyle has increased by 19% for a couple.

The “comfortable” lifestyle budget includes more luxuries, such as running two cars and three weeks visiting Europe each year.

For a two-person household, the cost of this lifestyle has increased by 10% in the last year.

The table below shows the PLSA’s estimated income needs for each lifestyle and how the period of high inflation has affected budgets.

Keep in mind that these figures are a useful indicator of retirement costs, but your outgoings will depend on your lifestyle. However, it does highlight why reviewing your pension and income is so important.

If you’ve already retired, you should look at whether you could use your assets to boost your income, while being mindful of ensuring you don’t run out of money during your lifetime.

4 things to consider if you’re reviewing your retirement income

If high inflation means you need to review your retirement income, these four questions could help you understand your options.

1. How much have your outgoings increased?

First, take some time to look at how your expenses have changed in the last year. While the official inflation figures can be useful, your personal inflation rate may be very different. It will depend on how you spend your money and your priorities. So, going through your budget could help you identify a potential shortfall.

2. What reliable income do you have?

In retirement, you may have several sources that you can rely on to pay an income for the rest of your life. This may include the State Pension, an annuity, or a defined benefit (DB) pension.

In some cases, the income provided will rise in line with inflation to protect your spending power. For example, the State Pension will rise by a record 10.1% in April 2023. As a result, your income gap may not be as large as you first think.

3. What other assets could you use to increase your income?

Next, review your other assets that could provide an income in retirement. This could include a flexible income from a defined contribution (DC) pension. You may also have other assets you could use, such as investments, savings, or property.

Reviewing these assets could help you bridge a potential gap if inflation means you’re facing a shortfall.

4. Could you sustainably increase your income?

Remember to look at your overall financial plan and consider the long term when making decisions.

While other assets could boost your income, don’t forget to consider whether using these assets is sustainable over the long term.

So, while you could increase how much you withdraw from your DC pension, could it mean you run out of money later in life? And how would taking an income from investments affect your portfolio’s performance?

Contact us to create a retirement plan

As financial planners, we can work with you to create a retirement plan that suits you. We’ll consider what type of lifestyle you want throughout retirement and how you could use your assets to help you achieve it. We’ll also factor in potential risks, such as a period of high inflation, so you can have peace of mind about your retirement finances.

Please note: This blog is for general information only and does not constitute advice. The information is aimed at retail clients only.

The value of investments and any income from them can fall as well as rise and you may not get back the original amount invested.

Past performance is not a guide to future performance and should not be relied upon.

Approved by The Openwork Partnership on 21/03/2023.