As you approach retirement, your attention may turn to your financial future. As you begin looking to gain clarity on your retirement, you might think about:

- When you might be able to retire.

- Whether you’ll have enough to support your retirement goals.

- What steps you need to take to ensure you have a sustainable income.

Read on to find out how we can answer your questions and develop a plan to help you enjoy the retirement you’ve always dreamed of.

Knowing how you’d like to spend your retirement

When you think about planning your retirement, your mind probably automatically jumps to your pensions, savings, and investments.

While this instinct is natural, it’s often wiser to first consider how you’d like to spend your retirement. Without knowing what your lifestyle will look like when you’re no longer working, it will be difficult to understand whether you’re on track financially.

Think about your priorities and the reasons you’re looking forward to this next chapter of your life.

According to research reported by Scottish Widows:

- 34% of people aged 65 and over plan to use their savings on travel.

- 14% of people aged 60 to 64 plan to buy their dream car.

- Other priorities included dining out, exercise, and treating loved ones.

All this to say, we’ll start by exploring your priorities for the future. Whether it’s travelling the world or focusing on what’s closer to home, we’ll help you get your goals in place.

Working out how much you’ll need to meet your goals

A 2025 Which? survey revealed that 49% of people lacked confidence about how much money they’d need for a comfortable retirement.

It can be tricky to calculate just how much you should be aiming for.

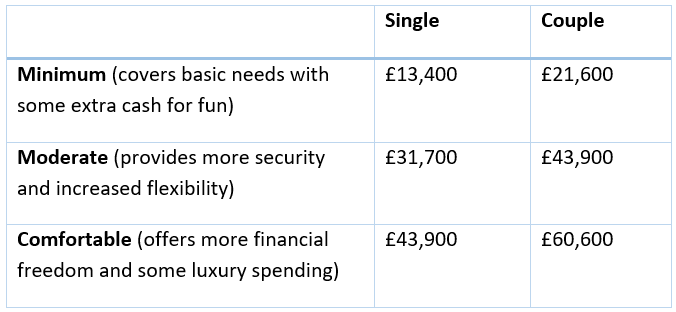

The good news is that Pensions UK has created three pillars to help you judge how much you may need, depending on whether you’re aiming for a minimum, moderate, or comfortable standard of living:

The amount of income you need in retirement will be specific to you and your goals, but this research may provide a useful starting point.

It’s also important to remember that your spending patterns will likely change as you age.

- On the go – During the early stages of retirement, there’s a strong likelihood that you’ll spend more on travel, hobbies, or home improvements.

- Slowing down – While you may be slightly less active, you’re still busy with hobbies, but you may be less inclined to long-haul travel.

- Coming to a stop – In later life, your mobility may be more limited, and you may require care.

Figuring out where your retirement income will come from

It can be hard to keep track of your pension. We’ll help you understand what you have in your pots and advise you on potential strategies to help you get the most out of your pension, including maximising schemes and utilising tax relief.

You may find it helpful to think about your pension income in blocks. Start with the State Pension, then consider your personal or workplace pensions, and then add any additional income you might get from other investments you hold or rental property you have.

State Pension

The full level of the new State Pension for the 2026/27 tax year is £230.25 a week, or £11,973 a year. However, you may not qualify for the whole amount. Visit the government website to find out what you can expect.

Final salary pension

Defined benefit (DB) or final salary pensions pay a regular monthly income, which is based on your earnings while you were working. Your annual statement will tell you how much you can expect to receive in retirement.

Defined contribution pension

A defined contribution (DC), or money purchase, pension is a savings pot you (and sometimes your employer) will have contributed to during your working life.

When you retire, you’ll need to decide how to draw an income from it. Although it’s possible to take the whole pension amount in one go, it could lead to a substantial tax bill, and you would be responsible for ensuring the money lasts for the duration of your retirement.

There are two popular ways to generate an income from this type of pension: income drawdown, or using the value of the pot to purchase an annuity. Some people opt for a combination of both.

Creating a tax-efficient income using all your financial sources

You may benefit from using other financial sources before accessing your pension.

While you may consider your pension as the foundation of your retirement plan, pension funds typically benefit from tax-free growth, interest, and dividends. So, leaving your pension invested could potentially help you to maintain capital value.

You also need to think about how to draw your income tax-efficiently, which we can also help with.

Visualising your financial future with cashflow modelling

Cashflow modelling can help you to see if your savings are sufficient to support you throughout your life. Your Financial Planner can input data such as your current assets and savings, key event dates such as your expected retirement date, and any financial commitments you have now, or in the future.

To forecast your future income, the software makes assumptions about the expected returns on investments, and how inflation might alter things.

By regularly reviewing your cashflow model, you will understand how much income you’re likely to need and, together with your Planner, you can decide the best options for accessing your pension.

It’s also important to be realistic about the amount of income you’ll need, including any later-life care costs, so that you can plan effectively.

We’re here to help you gain retirement clarity

It’s never too soon to plan for the future you want. There’s a lot to think about when you’re planning for your retirement, and it’s important to understand the implications of all your decisions.

We can talk you through all your options, helping you to gain retirement clarity so you can relax and enjoy the next chapter of your life with confidence.

To find out more, please email contactme@kbafinancial.com or call us on 01942 889 883.

Please note

This article is for general information only and does not constitute advice. The information is aimed at retail clients only.

All information is correct at the time of writing and is subject to change in the future.

The value of investments and any income from them can fall as well as rise and you may not get back the original amount invested.

Past performance is not a guide to future performance and should not be relied upon.

HM Revenue and Customs’ practice and the law relating to taxation are complex and subject to individual circumstances and changes which cannot be foreseen.

The Financial Conduct Authority does not regulate cashflow planning or tax planning.

Approved by The Openwork Partnership on 5/2/2026.